PDF document

About the program and evaluation

- RSF is a grant that is meant to offset indirect costs related to federally funded research and is not designed to fully support specific activities or projects.

- RSF invested $1.7 billion between 2013/14 and 2017/18, distributed to 139 institutions.

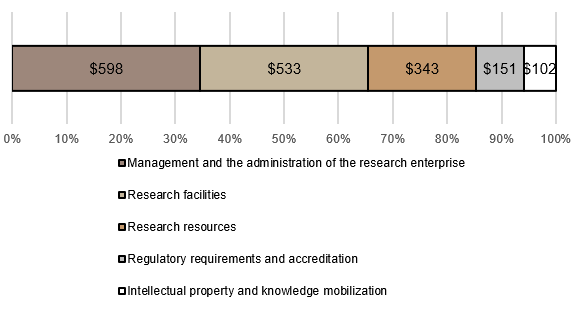

- Grants can be allocated to any of the five eligible expenditure categories: research facilities; research resources; management and administration of the research enterprise; regulatory requirements and accreditation; and intellectual property and knowledge mobilization.

- The scope of the evaluation covered the five-year period from 2013/14 to 2017/18 and focused on four questions.

Key outcomes achieved

Immediate outcomes

- The RSF program has continued to be successful in making a contribution to defraying indirect costs incurred by institutions as a result of federal investments in academic research.

Investment in each of the eligible expenditure categories

(Amount in millions)

Long description

Investment in each of the eligible expenditure categories

(Amount in millions)

| Expenditure category |

Proportion |

Amount (in millions) |

| Management and the administration of the research enterprise |

35% |

$598 |

| Research facilities |

31% |

$533 |

| Research resources |

20% |

$343 |

| Regulatory requirements and accreditation |

9% |

$151 |

| Intellectual property and knowledge mobilization |

6% |

$102 |

Intermediate outcomes

- Through interviews and surveys, institutions explained how these investments have contributed to the achievement of intermediate outcomes.

“Our university has seen steady growth in the square footage of research laboratories [….] The RSF is critical to supporting this increasing space through provision of maintenance, upgrades, utilities, etc.” (U15 institution)

Long-term outcomes

- The Research Support Fund is expected to optimize the use of federal direct research funding and contribute to the competitiveness of Canadian institutions on the world-stage.

“RSF funds are used annually to support positions within the research accounting team within finance. These positions are responsible for annual reporting to the tri-council thereby relieving this task from researchers or staff within faculties. Having funding to centralize this function allows for efficiency and effectiveness as the staff develop expertise at a level that a distributed model would not allow for as staff would have many other tasks not just research support and administration.” (Research-intensive, Non-U15 institution)

Key findings and conclusions

Evaluation Question 1: How have changes in the research environment impacted the need for RSF?

- Federal investments in direct research funding continue to generate indirect costs at institutions.

- The increased federal investments have been mirrored by increases in the RSF funds.

- Institutions appreciate the flexibility of RSF, allowing them to respond to local cost-drivers.

- There continues to be a need for a federal contribution that defrays these costs.

Recommendation 1: Continue to contribute financially to defraying the indirect costs of research associated with federal investments in research.

Evaluation Question 2: To what extent has the RSF contributed to effective use of direct federal research funding?

- RSF has defrayed indirect costs in the five eligible expenditure categories (immediate outcomes).

- RSF has made a contribution towards intermediate outcomes.

- The strength of the causality between the program’s immediate and intermediate outcomes have been overemphasized in the program’s logic model.

- Examples from institutions explained how the investments made in the expenditure areas contributed to RSF’s intermediate outcomes.

- Institutions’ perceived impact of RSF was generally high.

- The contributions could not be systematically quantified.

- A contribution towards effective use of federal funding was inferred (final outcomes).

Recommendation 2: Refine the program logic model to make it clearer that the program is only expected to make a contribution to the expected intermediate and long-term outcomes.

Evaluation Question 3: Has the RSF continued to be delivered in a cost-efficient manner?

- RSF has a low operating ratio which has decreased over time.

- Some concerns were raised regarding:

- the sufficiency of resources for program administration;

- the efficiency of the process used to calculate grant amounts, which resides at each of the three agencies.

Evaluation Question 4: How could performance information be collected (considering current challenges and barriers)?

- Larger institutions reported pooling funds with other operating funds, losing the ability to link RSF to specific eligible sub-categories or expenditures (e.g., number of FTEs, square footage of research lab space).

- Small and medium-sized institutions described expenditure tracking as easier as allocations were generally for one or two major functions (e.g., FTEs, a facility) and RSF’s relative contribution was higher.

- Institutions had difficulty reporting on the percentage of eligible indirect cost covered by RSF in the survey (could maybe report on the total indirect cost covered by RSF).

- The evaluation identified what performance information institutions said they could easily report on:

- whether or not the RSF funding supports salary in each expenditure category;

- possibly whether or not the RSF funding supported eligible sub-categories or expenditures;

- for each eligible expenditure area, examples of ways in which RSF funds contribute to the research enterprise.

- There continues to be a lack of consensus regarding what information should be collected and finding the right balance is complicated.

- Several factors need to be considered including the feedback from institutions, the risk associated with the program as well as management’s needs for performance information to support managing the program and meeting accountability requirements.

- The extent to which the current program design supports adequate performance reporting should also be discussed.

Recommendation 3: Implement institutional reporting that is appropriate for the contributory nature of the program, the risk associated with the program and the performance information needs of program management.